Every salaried individual, freelancer, and business owner in India needs to understand how income tax works to plan finances, maximise savings, and file returns correctly. India currently operates two parallel tax systems — the new tax regime (default since FY 2023-24) with lower rates but minimal deductions, and the old tax regime with higher rates but extensive deductions and exemptions.

This guide focuses on understanding income tax slabs in India for FY 2026-27 (AY 2027-28). Budget 2026 made no changes to slab rates — the structure introduced in Budget 2025 continues as is. We cover both regime tables side by side, salary-wise tax calculations, all key deductions under Section 80C and 80D, and practical strategies for how to save income tax India legally.

- New regime: Income up to ₹12 lakh is tax-free (₹12.75 lakh for salaried after standard deduction) Old regime: Income up to ₹5 lakh is tax-free (with rebate under Section 87A) New regime is the DEFAULT — you must actively opt out to choose the old regime Standard deduction: ₹75,000 for salaried employees under both regimes Section 80C allows up to ₹1.5 lakh deduction (PPF, ELSS, LIC, EPF, Sukanya Samriddhi) If your total deductions under old regime exceed ₹3.75 lakh, old regime MAY save more tax

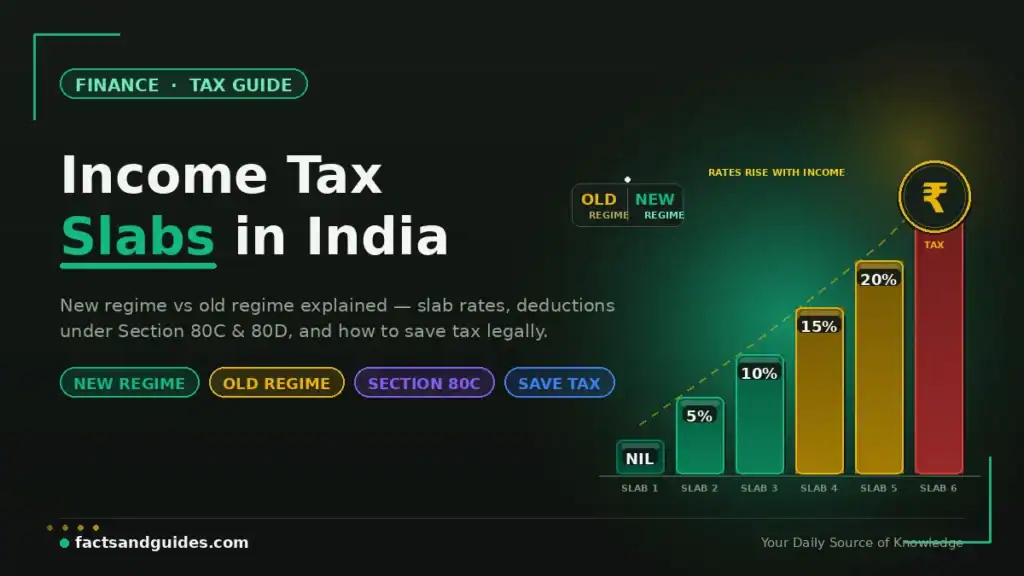

Income Tax Slabs 2026-27 India: New Tax Regime (Default)

The new tax regime is the default for all taxpayers from FY 2023-24 onwards. If you do not actively choose a regime, this is what applies to you automatically. Here are the income tax slabs 2026-27 India under the new regime.

| Annual Income (₹) | Tax Rate | Tax on This Slab |

|---|---|---|

| Up to ₹4,00,000 | Nil | ₹0 |

| ₹4,00,001 to ₹8,00,000 | 5% | ₹20,000 |

| ₹8,00,001 to ₹12,00,000 | 10% | ₹40,000 |

| ₹12,00,001 to ₹16,00,000 | 15% | ₹60,000 |

| ₹16,00,001 to ₹20,00,000 | 20% | ₹80,000 |

| ₹20,00,001 to ₹24,00,000 | 25% | ₹1,00,000 |

| Above ₹24,00,000 | 30% | — |

Key benefits of the new regime:

- Rebate under Section 87A: ₹60,000 rebate makes income up to ₹12 lakh completely tax-free

- Standard deduction: ₹75,000 for salaried individuals — so gross salary up to ₹12,75,000 is effectively tax-free

- Employer NPS contribution: Deduction up to 14% of basic salary under Section 80CCD(2)

- Health & Education Cess: 4% on total tax (no change)

- Marginal relief: Ensures those with income slightly above ₹12 lakh do not pay disproportionately higher tax

Understanding Income Tax Slabs in India: Old Tax Regime

The old regime has higher base rates but allows numerous deductions. For taxpayers who actively invest in tax-saving instruments (PPF, ELSS, NPS, home loan), the old regime may result in lower tax liability. You must actively opt for this regime — it is no longer the default.

| Annual Income (₹) | Below 60 years | 60–80 years (Senior) | Above 80 years (Super Senior) |

|---|---|---|---|

| Up to ₹2,50,000 | Nil | Nil | Nil |

| ₹2,50,001 to ₹3,00,000 | 5% | Nil | Nil |

| ₹3,00,001 to ₹5,00,000 | 5% | 5% | Nil |

| ₹5,00,001 to ₹10,00,000 | 20% | 20% | 20% |

| Above ₹10,00,000 | 30% | 30% | 30% |

Rebate: Under the old regime, Section 87A provides ₹12,500 rebate for taxable income up to ₹5 lakh — making income up to ₹5 lakh tax-free.

New vs Old Tax Regime India: Side-by-Side Comparison

This is the most important section for understanding income tax slabs in India — knowing which regime suits YOUR situation. Here is a clear new vs old tax regime India comparison.

| Feature | New Tax Regime (Default) | Old Tax Regime (Optional) |

|---|---|---|

| Basic exemption limit | ₹4,00,000 | ₹2,50,000 (below 60) / ₹3,00,000 (60–80) / ₹5,00,000 (80+) |

| Effective zero-tax income | ₹12,75,000 (salaried) | ₹5,00,000 |

| Standard deduction | ₹75,000 | ₹50,000 |

| Section 80C (PPF, ELSS, LIC) | ❌ Not available | ✅ Up to ₹1,50,000 |

| Section 80D (Health Insurance) | ❌ Not available | ✅ Up to ₹25,000–₹75,000 |

| HRA Exemption | ❌ Not available | ✅ Available |

| Home Loan Interest (Sec 24b) | ❌ Not available | ✅ Up to ₹2,00,000 |

| NPS Employer (80CCD(2)) | ✅ Up to 14% of basic | ✅ Up to 14% of basic |

| NPS Self (80CCD(1B)) | ❌ Not available | ✅ Additional ₹50,000 |

| Tax rates | Lower (5%–30% across 7 slabs) | Higher (5%–30% across 3 slabs) |

| Best for | People with minimal investments/deductions | People with heavy deductions (₹3.75L+) |

Tax Calculation at Different Salary Levels: Understanding Income Tax Slabs in India Practically

The best way of understanding income tax slabs in India is to see actual calculations at common salary levels.

| Gross Salary (₹) | Tax — New Regime | Tax — Old Regime (with ₹3L deductions) | Better Regime |

|---|---|---|---|

| ₹8,00,000 | ₹0 (under ₹12L limit) | ₹0 (under ₹5L after deductions) | Same — both zero |

| ₹10,00,000 | ₹0 (under ₹12L limit) | ₹31,200 | ✅ New regime |

| ₹12,00,000 | ₹0 (under ₹12L limit) | ₹72,800 | ✅ New regime |

| ₹12,75,000 | ₹0 (₹12L after std deduction) | ₹88,400 | ✅ New regime |

| ₹15,00,000 | ~₹1,09,200 | ~₹1,09,200 (with ₹3L deductions) | Approximately equal |

| ₹20,00,000 | ~₹2,73,000 | ~₹2,49,600 (with ₹4L deductions) | ✅ Old regime (if heavy deductions) |

| ₹25,00,000 | ~₹4,10,800 | ~₹3,74,400 (with ₹4.5L deductions) | ✅ Old regime (if heavy deductions) |

Section 80C Deductions India: Where to Invest ₹1.5 Lakh (Old Regime Only)

Section 80C is the most widely used tax-saving provision in India. It allows a deduction of up to ₹1,50,000 per year on specified investments and expenses. Understanding Section 80C deductions India is essential for anyone choosing the old regime.

| Investment/Expense | 80C Limit | Lock-in Period | Returns (Approx) | Risk Level |

|---|---|---|---|---|

| PPF (Public Provident Fund) | ₹1.5L (combined) | 15 years | 7.1% (tax-free) | Zero (Govt backed) |

| ELSS Mutual Funds | ₹1.5L (combined) | 3 years | 12–15% (historical) | Moderate-High |

| EPF (Employee PF) | ₹1.5L (combined) | Till retirement | 8.25% (tax-free) | Zero |

| Sukanya Samriddhi | ₹1.5L (combined) | 21 years | 8.2% (tax-free) | Zero (Govt backed) |

| NSC (National Savings) | ₹1.5L (combined) | 5 years | 7.7% | Zero |

| Life Insurance Premium | ₹1.5L (combined) | Varies | 4–6% | Low |

| Children’s Tuition Fees | ₹1.5L (combined) | — | — | — |

| Home Loan Principal | ₹1.5L (combined) | — | — | — |

| 5-Year Bank/PO FD | ₹1.5L (combined) | 5 years | 6.5–7% | Zero |

Other Key Deductions Beyond 80C (Old Regime)

| Section | Deduction For | Maximum Limit |

|---|---|---|

| 80D | Health insurance premium (self + family) | ₹25,000 (self) + ₹25,000 (parents) = ₹50,000. If parents are senior citizens: up to ₹75,000 total |

| 80CCD(1B) | NPS self-contribution (additional) | ₹50,000 (over and above 80C) |

| 80CCD(2) | Employer NPS contribution | 14% of basic salary (available under BOTH regimes) |

| 24(b) | Home loan interest (self-occupied) | ₹2,00,000 per year |

| 80E | Education loan interest | No upper limit (interest portion only) |

| 80G | Donations to approved charities | 50% or 100% of donation amount |

| 80TTA | Savings account interest | ₹10,000 |

| HRA | House Rent Allowance | Calculated per formula (varies) |

How to Save Income Tax India: 10 Legal Strategies

Here are 10 practical ways to legally reduce your tax liability — essential knowledge for anyone understanding income tax slabs in India and applying them to real life.

- 1. Max out Section 80C (₹1.5 lakh): Invest in PPF, ELSS, or Sukanya Samriddhi if you are on the old regime.

- 2. Buy health insurance (80D — up to ₹75,000): For self, spouse, children, and parents. Genuine health protection + tax saving.

- 3. Claim HRA if you pay rent: One of the largest deductions available to salaried individuals living in rented accommodation.

- 4. NPS contribution (80CCD(1B) — additional ₹50,000): Over and above the 80C limit. Builds retirement corpus + saves tax.

- 5. Employer NPS (80CCD(2)): Available in BOTH regimes. Ask your employer to restructure salary to include NPS contribution.

- 6. Home loan interest (Section 24b — up to ₹2 lakh): If you have a home loan on a self-occupied property.

- 7. Education loan interest (80E): No upper limit — the entire interest component is deductible.

- 8. Compare regimes EVERY year: Your optimal regime changes based on your deductions that year. Run both calculations annually.

- 9. Donate to approved charities (80G): Genuine philanthropy that also reduces tax liability.

- 10. File ITR even if tax is zero: A filed ITR serves as income proof for loans, visas, and credit cards — even with zero tax liability.

Many government schemes also provide tax benefits. Check our 15 Government Schemes Every Indian Should Know for more tax-saving options like Sukanya Samriddhi (EEE status) and NPS.

Surcharge and Cess on Income Tax 2026-27

| Taxable Income | Surcharge Rate (New Regime) | Surcharge Rate (Old Regime) |

|---|---|---|

| Up to ₹50 lakh | Nil | Nil |

| ₹50 lakh – ₹1 crore | 10% | 10% |

| ₹1 crore – ₹2 crore | 15% | 15% |

| ₹2 crore – ₹5 crore | 25% (capped) | 25% |

| Above ₹5 crore | 25% (capped) | 37% |

Health & Education Cess: 4% applied on (Tax + Surcharge). This is unchanged for FY 2026-27. The cess applies to everyone regardless of income level or regime chosen.

How to File Your Income Tax Return (ITR) for FY 2026-27

- Step 1: Gather documents — Form 16 (from employer), Form 26AS (TDS statement), AIS (Annual Information Statement), bank statements, investment proofs

- Step 2: Visit incometax.gov.in → login with PAN and password

- Step 3: Select the correct ITR form (ITR-1 for salaried individuals with income up to ₹50 lakh from salary, one house property, and other sources)

- Step 4: Compare tax liability under both regimes before selecting one

- Step 5: Fill details, verify against Form 26AS, and submit

- Step 6: E-verify using Aadhaar OTP, net banking, or DSC within 30 days

- Due date: 31 July 2027 for salaried individuals (non-audit cases)