Mutual funds have become the most accessible way for Indians to invest in the stock market — and you do not need lakhs of rupees or a finance degree to get started. In 2026, India’s mutual fund industry has crossed ₹68 lakh crore in Assets Under Management (AUM), monthly SIP inflows exceed ₹26,000 crore, and over 21 crore investor folios are active. Yet less than 5% of Indians invest in equity markets, according to the RBI’s 2025 annual report.

This beginner’s guide to mutual funds in India will take you from zero knowledge to your first SIP investment — step by step, in plain language, with no jargon. Whether you earn ₹15,000 or ₹1,50,000 per month, you can start building wealth with as little as ₹500.

- You can start a mutual fund SIP with as little as ₹500 per month (some funds allow ₹100) SIP automates investing — a fixed amount is debited from your bank every month India’s MF industry AUM crossed ₹68 lakh crore in March 2026 KYC is a one-time 10-minute online process — you only do it once Index funds (like Nifty 50) are the simplest starting point for beginners ₹5,000/month SIP at 12% for 25 years = approximately ₹1.9 crore

What Are Mutual Funds? Explained Simply

A mutual fund pools money from thousands of individual investors to invest in a diversified portfolio of stocks, bonds, or other securities. A professional fund manager — employed by an Asset Management Company (AMC) regulated by SEBI — makes all the investment decisions on behalf of all investors in the fund.

When the fund’s investments grow in value, so does your share. When they fall, your share falls too. You own “units” of the fund, and each unit has a daily price called NAV (Net Asset Value).

Think of it this way: if you cannot afford to buy shares of 50 different companies individually, a mutual fund lets you own a tiny piece of all 50 through a single investment. You get instant diversification, professional management, and SEBI regulatory oversight — all starting from ₹500 per month.

Types of Mutual Funds in India: Which One Is Right for You?

There are over 2,500 mutual fund schemes across 44 AMCs in India. That sounds overwhelming, but all of them fall into a few core categories. Understanding these types of mutual funds India offers is the first step to choosing the right one.

| Fund Type | What It Invests In | Risk Level | Ideal Time Horizon | Best For |

|---|---|---|---|---|

| Equity Funds | Stocks (large-cap, mid-cap, small-cap) | High | 5+ years | Long-term wealth creation |

| Debt Funds | Government bonds, corporate bonds, money market | Low–Moderate | 1–3 years | Stable returns, capital preservation |

| Hybrid Funds | Mix of equity + debt | Moderate | 3–5 years | Balanced risk-reward |

| Index Funds | Tracks a market index (Nifty 50, Sensex) | Moderate | 5+ years | Low-cost, passive investing |

| ELSS (Tax Saving) | Equity with 3-year lock-in | High | 3+ years (mandatory lock-in) | Tax saving under Section 80C |

| Liquid Funds | Short-term money market instruments | Very Low | 1 day – 3 months | Emergency fund parking |

Equity Funds — For Long-Term Wealth

Equity funds invest primarily in stocks. They carry higher risk but historically deliver the highest returns over long periods (5+ years). Sub-categories include large-cap funds (investing in top 100 stable companies like Reliance, TCS, HDFC Bank), mid-cap funds (companies ranked 101–250), small-cap funds (companies ranked 251+), and flexi-cap/multi-cap funds that invest across all sizes. For beginners, large-cap or flexi-cap funds offer the best starting point — good growth potential with manageable volatility.

Index Funds — The Simplest Starting Point

Index funds track a specific market index like the Nifty 50 (top 50 Indian companies) or the Sensex (top 30). They do not try to “beat” the market — they aim to match it. Their biggest advantage is extremely low expense ratios (as low as 0.05–0.20%), which means more of your money stays invested rather than paying fund manager fees. Many financial experts recommend index funds as the ideal first mutual fund for beginners.

Debt Funds — For Stability

Debt funds invest in government bonds, corporate bonds, and money market instruments. They are lower risk than equity funds and provide more stable, predictable returns (typically 6–8% annually). They are suitable for short-to-medium-term goals (1–3 years) or for the conservative portion of your portfolio.

ELSS — Tax Saving Mutual Funds

Equity Linked Savings Schemes (ELSS) are equity funds with a mandatory 3-year lock-in period. Investments up to ₹1.5 lakh per year qualify for tax deduction under Section 80C of the Income Tax Act. ELSS offers the dual benefit of tax saving and potential equity market returns — making it one of the most popular choices for salaried Indians. Learn more about tax implications in our guide on Understanding Income Tax Slabs in India 2026.

What Is SIP and Why Every Beginner Should Use It

A Systematic Investment Plan (SIP) is simply an automated monthly debit from your bank account into a mutual fund scheme of your choice. You pick a fund, choose a monthly amount (minimum ₹500, some funds allow ₹100), select a date, and set up a one-time auto-debit mandate. Every month, the amount is automatically invested — buying units at whatever the current NAV is.

SIP for beginners is the recommended way to start because:

- Rupee cost averaging: When markets are high, your SIP buys fewer units. When markets drop, it buys more units at lower prices. Over time, this averages out the cost and reduces the impact of market volatility.

- Discipline: Auto-debit removes the temptation to “wait for the right time” or skip months. Consistency is more important than timing.

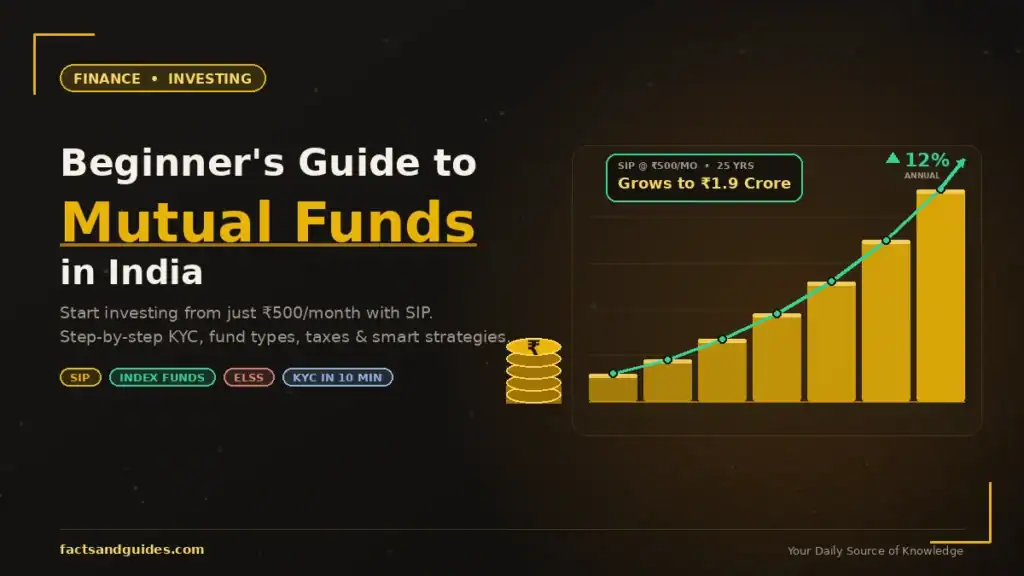

- Power of compounding: Small monthly amounts over decades grow dramatically. ₹5,000/month at 12% annual returns for 25 years becomes approximately ₹1.9 crore. For 30 years, it becomes approximately ₹3.5 crore.

- No timing needed: You do not need to predict whether the market will go up or down. SIP invests regardless of market conditions — and historically, this approach has outperformed most attempts at market timing.

| SIP Amount (₹/month) | Duration | Assumed Return (12% pa) | Total Invested | Approximate Value |

|---|---|---|---|---|

| ₹500 | 20 years | 12% | ₹1.2 lakh | ₹5 lakh |

| ₹2,000 | 20 years | 12% | ₹4.8 lakh | ₹20 lakh |

| ₹5,000 | 20 years | 12% | ₹12 lakh | ₹50 lakh |

| ₹5,000 | 25 years | 12% | ₹15 lakh | ₹1.9 crore |

| ₹10,000 | 25 years | 12% | ₹30 lakh | ₹3.8 crore |

| ₹10,000 | 30 years | 12% | ₹36 lakh | ₹7 crore+ |

How to Invest in Mutual Funds India: Step-by-Step Guide

Starting your first mutual fund investment is easier than most people think. Here is exactly how to invest in mutual funds India — from scratch, in under 15 minutes.

Step 1: Complete Your KYC (One-Time, 10 Minutes)

KYC (Know Your Customer) is a one-time verification mandated by SEBI. You need your PAN card, Aadhaar card, a bank account, and a passport-size photograph. Most platforms now offer instant e-KYC using Aadhaar OTP authentication — the entire process takes under 10 minutes. Once done, your KYC is valid across ALL AMCs and platforms in India. You never need to do it again.

Step 2: Choose an Investment Platform

Use a SEBI-registered, commission-free platform that offers “direct plans” (which have lower expense ratios than “regular plans” sold through banks or agents). The difference in expense ratio (0.5–1.5% lower) compounds significantly over time — potentially adding 15–20% more to your final corpus over 20 years.

| Platform | Best For | Commission | Key Feature |

|---|---|---|---|

| Groww | Complete beginners | Zero | Best user interface, very simple |

| Zerodha Coin | Investors who also trade stocks | Zero | Integrated with Zerodha demat |

| Kuvera | Goal-based planners | Zero | Advanced goal tracking, family accounts |

| Paytm Money | Paytm users | Zero | Familiar interface, easy UPI setup |

| INDmoney | Portfolio tracking across assets | Zero | Tracks MF + stocks + FD + EPF in one place |

Step 3: Choose Your Fund

For your first fund, keep it simple:

- Complete beginner with 5+ year horizon: Nifty 50 Index Fund (e.g., UTI Nifty 50 Index Fund — expense ratio 0.05%)

- Moderate risk, 5+ years: Large-cap or flexi-cap fund (e.g., HDFC Flexi Cap, Parag Parikh Flexi Cap)

- Want tax saving under 80C: ELSS fund (e.g., SBI ELSS Tax Saver — 3-year lock-in)

- Short-term parking (1–3 years): Debt fund or liquid fund

Step 4: Set Up Your SIP

Select your fund, enter your monthly SIP amount, choose a debit date, and approve the NACH/UPI auto-debit mandate from your bank. This is a one-time setup. Every month, the chosen amount will be automatically debited and invested. You will receive a confirmation with the number of units allotted at that day’s NAV.

Step 5: Track and Stay Invested

Monitor your portfolio through your platform’s app or through MF Central (mfcentral.com) for a unified view across all AMCs. Review once every 6–12 months, not daily. The single most important rule: do not stop your SIP during market crashes. SIPs actually benefit from dips because you buy more units at lower prices.

Mutual Fund Tax Rules in India (2026)

Understanding tax is essential for maximising returns. Here are the key mutual fund tax rules applicable as of FY 2026-27:

| Tax Type | Equity Funds (held >1 year) | Equity Funds (held <1 year) | Debt Funds |

|---|---|---|---|

| Capital Gains Tax | LTCG: 12.5% above ₹1.25 lakh | STCG: 20% | Taxed at your income tax slab rate |

| Tax-Free Limit | First ₹1.25 lakh LTCG is exempt | No exemption | No exemption |

| Section 80C Benefit | ELSS only — up to ₹1.5 lakh deduction | — | — |

7 Common Mutual Fund Mistakes Beginner’s Must Avoid

Mistake 1: Waiting for the “Right Time” to Start

There is no perfect time to start a SIP. The best time was 10 years ago. The second best time is today. SIP’s rupee cost averaging handles market volatility automatically — that is its entire purpose.

Mistake 2: Stopping SIP During Market Crashes

This is the biggest wealth-destroying mistake. When markets fall, your SIP buys more units at lower prices — this is exactly when SIP works hardest for you. Stopping during a crash locks in losses and removes the benefit of buying cheap.

Mistake 3: Chasing Last Year’s Top Performer

A fund that delivered 40% last year is not guaranteed to repeat that performance. Past returns do not predict future results. Choose funds based on consistent long-term track records (5–10 years), low expense ratios, and alignment with your goals.

Mistake 4: Investing in “Regular Plans” Through Banks

Regular plans charge higher expense ratios (typically 1–1.5% more per year) because they include distributor commissions. Over 20 years, this silently costs you 15–20% of your final corpus. Always choose direct plans through zero-commission platforms.

Mistake 5: Not Having an Emergency Fund Before Investing

Before starting any SIP, ensure you have 3–6 months of living expenses saved in a liquid fund or savings account. If an emergency forces you to redeem your equity SIP at a loss, the entire exercise becomes counterproductive.

Mistake 6: Over-Diversifying Into Too Many Funds

Owning 10–15 mutual funds does not equal better diversification — it creates overlap and confusion. Most beginners need just 2–3 funds: one equity (index or large-cap), one for tax saving (ELSS if needed), and one for emergency parking (liquid fund).

Mistake 7: Checking Your Portfolio Daily

Markets fluctuate daily. Checking your portfolio every day creates anxiety and tempts you to make emotional decisions. Review once every 6–12 months. SIP is a long-term strategy — let compounding work in the background.